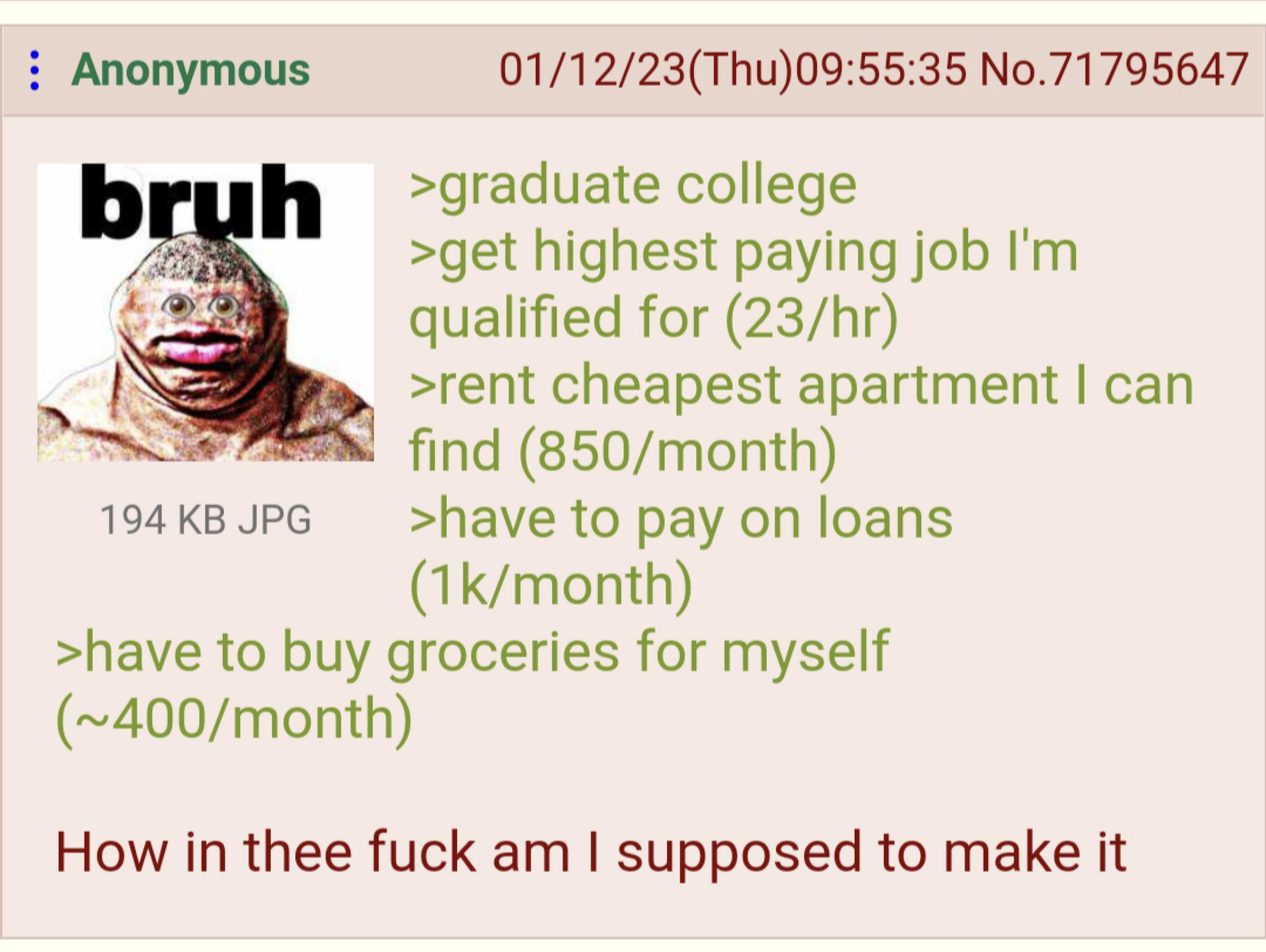

If we take out 7k of the gross $46,0000/yr for healthcare and retirement…

$5,700 for federal taxes, another k for state taxes…

That’s about $2692 a month, net. Subtract the just over $2k a month listed, there’s another $400 a month for… Utilities, phone, transportation, entertainment, savings, emergencies.

Even as rent is under 25% of income, pretty tight. Doable. But very tighter. You will never retire saving $4000 a year. You can never get sick. You apparently walk to work.

Pretty much have to get a roommate until the student loans are paid off.

Or start working crazy overtime.

And die.

Death is inevitable. 😃

But time is what we can change

Yeah, there’s no ‘supposed to’ – it’s not designed

It’s designed to prevent savings and use as much of your income for trickle up economics as possible before your max out your borrowing potential or get sick and die.

Talk with the student loan provider. Get on income based repayment plans, you end up paying more in the long run, but less each month (or none at all) so you can at least eat.

Is $1k/month student loan repayments in America usual?

This was nearly 20 years ago, but when I dropped out (two years in college, so don’t even have a degree), it was all spread across 4 loans (something weird, I dunno, I was a kid, but it was like a new loan for each semester? That didn’t even count the parent loans my mom took out for my schooling - thank god they just wrote those off entirely when she died). The repayment ticket book I received was $55 per week for each loan. That was $880 a month they wanted. For about a total of $50k of debt. With the sharp increase in tuition costs since I was in school, I wouldn’t be surprised if $1000 total per month is on the low end if you just pay what they ask you to. They don’t really tell you that you are taking out multiple loans by going to school, not just one big one.

I did as the above comment said and got on an IDR (Income Driven Repayment) plan, it basically refinanced my 4 loans into 1 and my monthly bill was now $57 a month, and it adjusts each year around tax time based on the previous year’s income. I’m currently paying about $80 a month.

That sounds like it sucks, especially to take on when you still don’t know what you are doing in life. I am glad you have since sorted it to be lower.

Do you get the same situation over there where interest increases the size of the loan more than you can pay it off with the lower amount now? In the UK most students expect to never pay theirs of before it gets cancelled around retirement age.

Yeah, I don’t know about their loan specifically but that’s a situation that happens here too.

We’ve killed the retirement industry and it just hasn’t hit yet.

Uhhh… In theory, if you are on one of the IDR plans, it is supposed to work that anything you have not paid off after 10 years gets “forgiven”… But I don’t even know if these plans existed 10 years ago, I think the one I am on was an Obama era program. I know there are a lot of government programs that are supposed to “forgive” some amount of the loan, or the entire loan, after a certain amount of time for people working in certain sectors (like teachers or other civil servants) that just aren’t actually working. I didn’t get on the program right away (I just let them ruin my credit for a decade…), so I’m not 10 years in yet (also because everything was on “pause” during covid from mid 2020 until late 2023, so those 3 years didn’t count toward the 10).

There have been news stories of people whose loans were supposed to be forgiven under one of those “civil servant” programs (because apparently we know they are horribly under-paid but instead of fixing that, we just made a program to forgive their massive student debt?) that just didn’t. The departments that handle the forgiveness play the “we are short staffed and too backed up, we will get to you eventually” card and they keep receiving bills every month, or they say their records don’t agree that they qualify anymore (blah blah whoopsy poopsy, you know how bad the gov’t is at keeping records, right?). And since the plans are usually dependent on not missing payments, you have to keep paying or risk losing the status needed for the forgiveness in the first place and/or they absolutely won’t forget to ruin your credit and fast.

It is a fucking nightmare all around to be honest. But at least it isn’t constantly ruining my credit anymore and I can afford to pay what they want each month without giving up on food or rent.

That’s much higher than normal. A quick google suggests between $200-$500 is more in line with a normal student loan monthly payment, which is still a burden on someone just starting out.

Only speaking from my own experience, but that sounds in-line with what the monthly payment is for each loan, but when I came out I had 4 separate loans that they came collecting on.

If you have any hope at all of keeping the interest from ballooning the principal beyond the original loan amount, yes.

:(

Or do what my cousin did.

Have uncle take out loan entirely under his name.

Make minimum payment on it.

When he dies, the debt dies with him.

How are they taking out education loans in someone else’s name? Sounds like fraud.

In the United States, there’s a federal loan option called Parent Plus loans that can allow parents to take out loans for their children’s education. Private loans could be taken out by just about anyone to pay for a student’s education, depending on the institution.

deleted by creator

The educated kind of fraud 🧐

A regular work day for corporations.

Parent loans are a thing. The parent of the kid takes out the loan, not the kid themselves. And yes, thankfully, they just go away if the parent dies and don’t get passed on to the estate.

edit Didn’t mean to double post the same comment - internet at work sucks :(

My daughter went to one fucking semester and is paying $900/mo for two years. We tried to talk her out of it but she wouldn’t hear reason. She’s going to go back to school a little wiser next year.

If you pay that much what is the sum of the loan? How much is a semester?

mine is like 280/mo, and my wife’s is like 175/mo. i think 1k/mo is very unusual

I got through college with no loans. But I had a scholarship for a few years that paid 75% tuition. I ended up taking 7 years to graduate because when the scholarship ran out, I cut back on my class load to work full time as a bookkeeper to pay for my living expenses and tuition. I could’ve done a lot better if I had gone to a community college for at least the first two years but I got duped by university “prestige”. Being in the workforce now, I know employers don’t care what school you attended.

numbers don’t check out

lists $2250 expenses… 100 hours of work per month would cover it

I know they have other expenses, but they failed to list them and failed to make their point.

100 hours of work if the money is tax free (it’s not). Taxes take about 40% of your gross income so on $23/hr hr can’t afford the listed bills.

By my estimation and IRS calculator, his tax liability is probably under 20%. Probably. This assumes about 15% is being taken out for healthcare and retirement however, so yeah, the net paycheck will be approximately 30-40% lower than gross.

I’d estimate OP has $440 a month left over after all the list expenses.

$440 per month to pay for gas, utilities, phone bill, insurance, incidentals, etc. You can forget about savings completely.

I don’t think OP is too far off the mark.

Use this tax calculator; it includes FICA, state taxes, and local taxes:

https://smartasset.com/taxes/income-taxes

No one is paying 40% total tax rate unless they are single, make $350,000+, and live in a high tax area (NYC, San Francisco). If you are married, you have to make at least $800,000 to pay 40% overall.

That’s what I used. Still some question about how much nontaxable retirement/Healthcare as well as what the state taxes would be. I estimated $5,700 in federal and $1000 in state. Based on 10% to retirement and $2400 a year for insurance, right off the top, and a 3% state tax.

I want a single bedroom apartment for 850.

You can get one a lot cheaper than that, but you’re going to have to move somewhere you probably don’t want to live.

And lose the money you save on fueling your car?

It kinda depends where you live, the cheaper apartments here are the same distance to work, just on a different side of town.

It’s still not worth the grief to live there, for me personally.

I live near one of the worst Philadelphia suburbs to live in (Chester) and even there you’re not going to find a one bedroom apartment for $850. You might find a room in a house for that little. On the flip side, I own a small two bedroom house in a very nice suburb that I rent out for $1400 a month. If you can find at least one other human being that you can cohabitate with peacefully, you can do a lot better than trying to find your own place. Easier said than done, I know - I hate living with other people.

Yeah before I got married I had housemates. It sucks but our rent was $750/month for a disgusting 2BR in a bad neighborhood 30 years ago when I was making $6/hr. That’s why I moved out of California.

In Russia we have plenty of single bedroom(they are just called single room) apartments for rent much less than 850. Even in Moscow.

Also don’t be worse than Russia. Please fix.

The old USSR did an excellent job of surveying the future population demands and building housing accordingly. This was called Central Planning and Americans scoffed at it as a thing that couldn’t work, because it didn’t immediately and immensely enrich the landed class.

Then the USSR collapsed, the Russian economy went into a nose dive, and Russia experienced an enormous population contraction as mortality rates and emigration surged. Suddenly, they had more housing stock than they knew what to do with, and even the newly implemented property class couldn’t squeeze people on the scale of your average Trumpy New York / LA / Dallas landleech. So now you’re still wildly overpaying what you’d have spent on housing thirty years ago, and the conditions have only deteriorated since. But you’re still somehow better off than some poor sap living in a Detroit slum or a San Fransisco closet or a Miami favela, paying twice as much.

These conditions aren’t going to last in Russia. But as Putin pivots back to a more command oriented economy (trading out old school soviet internationalism for new school national socialism) it does appear they’re positioned to avoid the American Techbro system of “Everyone must live in the pod and eat the bugs” that we’re currently headed towards.

The old USSR did an excellent job of surveying the future population demands and building housing accordingly.

Indeed. What USSR did really well is housing, healthcare and education. And looked into future. “We need to build school here because 30 years later current kids will have X kids that need to go to school”. Not that it didn’t have own downsides.

These conditions aren’t going to last in Russia.

I have to agree here for now. Degradation of education system is glaringly obvious. Healthcare in regions too. Housing… slowly deteriorates.

But as Putin pivots back to a more command oriented economy

Except Putin’s command economy will exist only to build more yachts for him and his oligarchs.

Not that it didn’t have own downsides.

Not unreasonably, people in these very structured economies would balk when they felt they were on rails heading into a profession or career that lacked prestige or a high quality of living. Everyone wants to be the company boss, nobody wants to be the guy working the line.

Except Putin’s command economy will exist only to build more yachts for him and his oligarchs.

Hardly. One of the critical impacts of sanctions on the Russian economy have been a deficit of luxury goods. But they’ve got tons of legacy capital from back when they used to make shit and export it to their allies abroad. Russian commercial airlines may become a thing again. Russian automobiles already are. And there’s quite a bit downstream in the economy that’s very lucrative to produce without needing to be larcenous.

The string of wars Putin’s getting his country into makes these kind of industrial centers vital. He doesn’t have the luxury of building yachts.

$23/hr x 40 hours = $920/wk

$920 x 52 weeks per year = $47,840 per year, gross.

government takes ~25% in taxes leaving you with net $35,880

rent is $850 x 12 months = $10,200

$35,880 - $10,200 = $25,680

student loans $1000/mo x 12 months = $12,000

$25,680 - $12,000 = $13,680

groceries $400 x 12 months = $4,800 $13,680 - $4,800 = $8,880 to spare.Your annual budget has a surplus of $8,880

Divided over 12 months, you have an allowance of $740 per month.Honestly you have it better than most people.

Furthermore you don’t need $400 in food each month.

Food is stupid anyway; Most Americans are overweight, so you can probably get by on less.

If carbohydrates have not yet been made toxic to your biochemistry via your metabolism being turbofucked to hell by sugar and empty starch, you could pull the red beans and rice plus basic spice hack for staple nutrition. Literally just big fucking bags of dry brown rice and dried red beans.

I see dried red beans and dry brown rice coming in around $1 per lb, and that’s DRIED remember - after you soak them and cook them you’re getting multiple pounds of food per dollar. You could get your grocery budget down to $100 per month if this is your base-load calorie source per meal and you decide to spruce things up every so often with a dollar here and a dollar there.

What about being happy for this money? Can you have a fulfilling life for 740 bucks a month? What if you subtract bills from it first? What if you subtract transportation costs, seasonal clothing, repairs, medical bills? Can you feel happy if you worked your ass off to get a good job in your field only to have to eat beans and rice and have fun for free or at home?

Looool work 40/52, shut up and eat ur beans, bitch

Seriously, in the face of technological efficiency of the 21st century your answer to that life-situation is smth smth carbohydrates?

Utilities? (ie water, power, trash)

Phone. Internet. I guess you could always attach your ethernet strait into the red beans and rice.

Car payment…

Insurance…

Gas…

You got gas covered too, with the beans there…

The system has made it impossible to live alone. You pretty much have to pair up with someone and split finances, whether that’s a romantic partner or a roommate or whatever. You have to be absolutely killing it to be younger than 40 and living alone right now.

American Capitalists: “Communism doesn’t work.”

Also, American Capitalists: “Live in a large shared space, cook meals together, and maybe even do a little farming on the side to supplement your diet. Also, don’t use the traditional professional trade system. Learn by doing! Become your own mechanic, have friends cut your own hair and do your own dentistry, home school your kids, and dig your own well for water. Basically, become a 1950s Maoist.”

23/hr at full time work (40 hrs/week) is $920/week.

Let’s assume that 15% is taken out of each paycheck for taxes and withholdings and such, which leaves $782.

A typical month has 4 weeks, so $3128/month.

Stated expenses are $850+$1000+$400 totaling $2250

$3128-$2250=$878

bruh, if you’re not making it with that kind of money, you need to take a serious look at your finances and cut back on things you don’t need.

EDIT: I’m not replying to everyone.

There are several expenses that would be expected that were not covered. Those should easily fit inside the $878 monthly fund. I’m not going to go through item by item because they weren’t mentioned by OP and everyone will have a different list. The things I’d put on the list absolutely fit, with plenty to spare.

The tax rate is based on my personal experience of being poor in Texas. This was a bit of an asspull, but I did math last year that determined I was losing 13% of my paycheck to taxes and withholdings, and I make a bit less than OP so I bumped it up a couple percent. Texas does not have state income tax, so if that number sounds low that’s probably why.

Ultimately, I stand by what I said.

Expenses a normal person would likely have that aren’t mentioned:

- car related expenses

- utilities, if not covered by rent (especially a cheap apartment is unlikely to cover all the utilities

- any needed insurance not covered by job

- savings

- less frequent necessities (clothes, tools, repairs, medical expenses)

- ideally a little money for something enjoyable every once in a while

Plus what lawless hellscape is 15% for taxes and withholdings? In Ontario you’re paying 20% for taxes alone at the absolute minimum. That’s not including CPP, EI, and anything else you have like benefits co-pay or union dues.

The country is probably America, and the state is likely a red one. And you’re right about lawless hellscape. We have states that don’t collect income tax, 9 of them as a matter of fact. But they still pay federal income tax, which is the lions share of taxes.

I’m not even in one of those states, and for the majority of my working life my withholding has been about 15%. But, I wish I could pay 5-10% more in taxes for some universal healthcare. My employer pays about $10,000 a year per head for our premiums, which is very kind of them because they don’t have to pay 100% of the premiums. And that wonderful healthcare plan is a “zero deductible”, but not like you’re thinking. No, the plan pays absolutely none of your medical bills or visits or prescriptions until you hit your yearly out of pocket, which is $9,000 in network, double that for out of network. What percent of my income do you think $19,000-$27,000 is? I’ll give you a hint, it’s more than 10% haha.

Oh, the cherry on top… The only urgent care facilities in my area that are in network are owned by one hospital group. They stopped doing walk in visits. You have to schedule “urgent” care days in advance or go to one of their “standing emergency room” clinics that are minimum $1000. They invented a new, more expensive tier of urgency in between urgent and emergency. I think this is what they mean when they say capitalism breeds innovation.

Your comment is the biggest problem we have right now. There’s no, just paying a little more on taxes to get free healthcare. It’s estimated that currently it would be $3-4 trillion a year for universal healthcare. The total taxable income the US made was ~$4.4 trillion. 41.5% of that is individual taxes. If everyone paid 10% more that would only be $182B. You haven’t even scratched the surface of the cost. Adding universal health care is far more complicated than just everyone paying a little more in taxes.

Somehow only almost every other first world nation has figured it out, must be that American exceptionalism preventing us from figuring it out.

Also, I think you misunderstood my increase statement. I don’t mean a 10% increase of the federal taxes, I mean a 10% additional tax on total income which is about 10x that. Even using that figure, you’re really telling me that it would take a 24% increase to pay for this, and I’d love to see your sources for that.

And, this is fun, even with your tax increase requirement numbers, $18,000-$27,000 is 24%-37.5% of the median household income in America. Turns out, even if it were as absurdly expensive as you say, it’s literally a bargain for your average family. I now make more than the median, and it’s only 20%-30% of my income, so still a bargain but not as good of one.

Are you saying that paying 30% of your income for free health care is a bargain? At the median income for 60 years would be almost $1.4MM.

Man, that sounds like the worst case, Ontario…

Attodaso man, fuckin attodaso.

Texas governments (city, state) makes money from sales and property taxes. The payroll taxes are federal.

OP didn’t mention a car, unless they live in an area where it is somehow required, they might just go without one for now

I don’t understand why this has so many down votes, it’s correct! To have $878 available monthly I’d need to move back in with my mom (aka free rent and occasionally food too). And I’m a junior softer dev, easily among the higher paying jobs for starters. That’s some killer money if you got your own place on top, also spending 400 on food? Holy sheep shit.

It’s not even slightly correct.

- Estimate of taxes & withholdings is way too low. Maybe some states have such a low tax rate, but most places do not. In addition, withholdings are usually much higher.

- There are tons of expenses not itemized that you can assume most people will have. Phone, internet, utilities, renters insurance, health insurance, car payments, gas, car insurance, parking, transit tickets, bank account, etc.

- Also doesn’t account for an emergency fund, savings of any kind or anything other than hand to mouth.

- Then there’s stuff you need to keep your job & apartment. Cleaning supplies, soap, deodorant, shampoo, laundry soap, dryer sheets, garbage/recycling/compost bags, clothes, shoes, haircuts etc.

- God forbid you have any sort of uncovered medical expenses. Birth control, OTC drugs of any kind, glasses/contacts, supplements for some kind of nutrient deficiency, dispensing fees for prescription drugs, etc.

Why do people insist on dragging each other down like this, like some billionaire is going to be impressed with how long they were able to live off a sack of rice and beans.

It costs nothing to support each other.

This isn’t about dragging each other down. Those are genuinely the costs of living for me (central Europe). 15% is the tax rate, the only time I payed more than 400 bucks for groceries in a month was when me and my gf together bought take out every day because we were in the process of moving among other things, and there’s no way in hell our internet/electricity/water/gass bills could put a major dent into 878 bucks. That shit is like 150, where we often pay reserves, so a small chunk of that will come back.

America is fucking expensive if that’s true, like holy shit, good luck to you all. It’s easy to forget that in America you’re forced to buy a car and pay for healthcare (here, health care is part of the 15% tax btw). Here you can just buy a YEARLY public transit ticket for around 150 (more for nationwide, but whatever) and just rent a small van when you really need a car. Altho I ear a little less than OP and still manage to squeeze in a small cheap car. And with my gf doubling our income we can even afford a bit larger flat. I’d argue I’m quite spoiled and not using my money effectively and still manage fine.

it’s because it’s not taking into account any other expenses, phone, internet, utilities etc.

Spending 75-100 a week for a person in groceries is pretty normal in my experience. Before COVID I was spending 50-60 a week but those days are over. .

I’m realistically in the situation OP is trying to get at. I’m making over $30/hr, I’ve been in my career a few years. I pay $1500 towards my housing expenses each month (rent/mortgage, electricity, heat, etc). I pay something like $500 in insurance between my vehicle and home, probably a bit less… My debt repayments are well over $1000/month. I pay $100 each for my cellphone and internet…

I have a slew of other expenses I can’t really enumerate. When I factor in food and gasoline, etc, I basically have no money left. I might have $200 left each month if I’m very thrifty with food.

You know what I’m doing? I’m in the process of getting my finances into a system that can help me visualize the spending and plan for my month over month budgeting. I’m trying to find where I can find costs I don’t need, and cut costs where I can. My work requires me to have a car, and while my vehicle is older, it works great and is pretty good on gas; best of all, I’ve paid off my car. I’m trying to dig myself out of this situation I’m in, and get in the black eventually. I’m tired of worrying about debt, which I’ve been in for nearly 20 years, in some way, shape or form.

I use ynab (you need a budget) to try and help me out. Emphasis on try.

Solid suggestion. I’m trying to get up and running with something a bit more involved. Right now I’m standing up a firefly III system for myself; I have to stand up an add-on to import data. Still gotta figure out some particulars.

It’s self hosted FOSS, which bluntly, I trust more than anything else. I’m certainly not paying what some companies think their budgeting software is worth on a subscription just to do my personal finance.

EDIT: just to be clear, I’m not knocking the price of ynab here, I’m more specifically talking about something like quicken, which is between $2-5 monthly to subscribe (depending on which product you get). IMO, it’s pretty idiotic to pay monthly to manage your monthly finances. I would imagine most people would use quicken (or a similar app) to reduce their month by month spending on stuff, and the first thing you need to do to get started is to spend more money monthly to have the privilege of doing so. There are obviously benefits and value to doing that, but it doesn’t make sense for me.

If you don’t need a ton of data, Mint mobile has a $15 a month 5 GB per month plan. It costs me $201.51 per year. I have to pay a year at a time, but that helped me cut my phone costs by a ton

Heh. I’m Canadian, our telecom situation suckkkks

As an American, I’m terribly sorry for what we exported politically to your country.

I don’t hold you, or any Americans, personally responsible. I understand that there’s a certain culture in your country… Not the primary culture, there’s a mash of a few different cultures, but one specifically (you know which one), that’s particularly problematic.

That culture has infected us for seemingly no good reason whatsoever. A lot of the issues that are central to that culture are not even discussed in our political circles because they’re issues we’ve basically decided on already, that, with any luck at all, will not be changing.

Those up here that have tried to stir the pot have so far, gotten nowhere.

The most significant impact that I’ve directly been aware of from American politics was the mask protests. The idiot bridge that decided to have a demonstration at the capital during COVID, ironically leading to several of them getting COVID in the process…

It’s not just the anti mask protests I’m taking about, it’s the group that would have a protest about mask mandates. IMO, they’re the most direct and significant problem to be inherited from our neighbors to the south, and bluntly, I don’t consider them a representation of the nation as a whole. For the most part, like Canada, you’re all just regular people living your lives trying to make it by. Not deranged activists trying to prove a point that everyone understands and thinks you’re an idiot for dying on that hill… Oh we know what their point is, we just don’t care, nor agree with it.

I’m sure most of our neighbors to the south are just trying to get by without struggling too much.

I’m certain you’re mostly all fine folk just trying to live.

Do you pay 500$/month on insurance? Or was that a typo?

Just about. I have pretty comprehensive insurance on my car, plus content and property insurance for my home.

All average between $100-$200 each, so $500 is a reasonable estimate.

That is crazy to me. I pay something like 500€/year for house insurance including contents and about 400€/year for the car. So that’s about 75€/month. But I’m in a different country so who knows. Your other expenses weren’t that different to mine, though.

I’m in Canada so our dollar is worth less than American dollars and I believe euros are with more than USD, works out to 330 euro or something.

Our rates are clearly higher still. But hopefully that puts things into a better context.

I’m around $35 CAD for my wage per hour, which is still pretty low IMO.

Inflation has hit us really hard…

You have nothing to lose, but your chains.

Thats the neat thing, you’re not!

If anon is in the US, they can switch to a SAVE plan which would make their monthly payments zero and get the loan discharged after 20-25 years. It’s not much, but it’s something.

Can you explain a bit more for us non-americans? You pay 0 and after 25 years it’s written off? Why doesn’t everybody do that then?

You pay a percentage of your income, but 225% of the federal poverty guideline is subtracted from your income before the calculation is made. If you haven’t paid off the loan within a certain timeframe (I believe 10 years if you have $12,000 in loans or less, 20 years if it’s more but you didn’t go to grad school, or 25 years otherwise) the loan is discharged, but you have to treat the discharged amount as taxable income for the year it’s discharged. Also, if you make your monthly payment ($0 for anon), your loan doesn’t accrue interest that month.

Ah ok that makes more sense, thanks for explaining!

deleted by creator

Spend less on candles.

Removed by mod

My parents convinced 17 year old me that I would be stuck flipping burgers if I didn’t go to college and get good grades. I went to college and got good grades. Now I can’t get any job.

The employment market is super tight right now. A year ago I was freshly graduated after returning to college and landed multiple interviews as well as fending off headhunters on about a weekly basis. I applied to 9 openings and got 6 calls to interview, and made it to the final round of interviews for 3 roles in a 1 month timeframe. Now I’m fighting just to get an interview for the purposes of interview experience and potentially jumping ship if the offer is right, and I’m getting ghosted by the couple of recruiters who have reached out in the last few months. A friend’s boyfriend is job hunting after getting laid off from his last job and hasn’t been able to land a job in months, and another friend landed a job with an insane commute after her position was suddenly no longer needed. Even my old boss who I see at community events regularly and has been begging me to come back and throwing comparatively generous offers out there hasn’t brought it up in a few months. Shit’s rough yo

I was never able to find a stable job, and I graduated in 2019. Went back for a master’s degree, which I just finished in March. There’s nothing. I’m about to run out of money. I don’t know what to do, but I can’t survive in this economy with no help.

deleted by creator

Removed by mod

It sure would be nice to have more open minded, diverse people working blue collar. It’s exhausting quietly listening to all these conservatives at work and feeling like I’m the only one who gives a damn.

deleted by creator

same with public school custodial dept. i make over 20 an hour with no degree. but I’m pretty capped now because I’ve been here 7 years and the union isn’t strong enough to leverage the QOL raises we need and deserve.

i highly prefer blue collar but I also have medical limitations and there’s just not enough regulation for things like extreme heat in these physical type jobs, which has kept me from seriously considering working construction.

Society paid for my lengthy uni education so joke’s on them. But I am sorry for people who get absolutely ripped off in other countries like the US etc.

Vocational stuff should definitely get an equal footing with academics.

Plumbers, electricians, etc.

They don’t because universities are absolutely rinsing it on the tuition fees.

people need to stop going to college if there is no monetary benefit to going

Setting aside the idea of going to college for personal enrichment and social development (really fucking important life skills that have long term but difficult to explicitly calculate monetary benefits), its very difficult to say whether a particular college degree in 2024 will pay dividends by 2044.

I’ve seen more than a few people poo-poo English degrees, but when a college degree is functionally mandatory for any kind of corporate employment that’s obviously not true. I’ve seen people laud STEM degrees, then go off and work in the Fivr mines for years earning less than they’d get in a mediocre Sales & Marketing gig (which you can score easily with any kind of BA). I’ve seen people talk up vocational training, but so much of that hinges on your employer and the state of the industry at any given moment (roofers and plumbers doing great in Houston right now, but that’s because home owners’ insurance hasn’t completely abandoned the state yet).

I initially tried the “no degree” route and quickly observed the very low ceiling to what I could earn without a degree while working the white collar jobs that I’m good at, as well as how difficult climbing the ladder beyond that is. The pay bump and quality of work benefit from just a 2 year degree has been incredible

Removed by mod

{kind=link}